Jamie Goldstein

Jamie GoldsteinLike most venture capital firms, we began life at Pillar investing in equity. Sometimes in a convertible note or a SAFE, but always with an eye toward converting into equity. We’ve spent years focused on traditional metrics — pre-money valuations, revenue, profits, cash flow, gross margins, capital intensity.

But times have changed, and our thinking has had to change along with it.

We made our first blockchain investment in a company called LBRY in mid-2016 — we purchased a note that would convert into equity. LBRY aims to be the decentralized version of YouTube, creating a direct relationship between content producers and viewers, removing the middleman and giving more control and economics back to the participants. We thought the application was interesting, we wanted to learn more about blockchain and we really liked the founder, Jeremy Kauffman. Beyond that, we didn’t know what we didn’t know.

LBRY’s plan included the creation of a crypto token, LBC (LBRY Credit) to power the network. Users would buy tokens or earn them by watching promoted content or inviting friends. Content owners set their own prices and were paid in tokens. Miners and hosts rewarded with tokens. Growth in the network should result in growth in demand for tokens and an increase in token value.

Earlier this year, we noticed a sharp rise in LBC value and trading volume. The company never did an ICO, the tokens were in the market through what would today be called an “airdrop”. LBRY, the company, was suddenly sitting on hundreds of $M worth of credits. Trading volume of LBC on popular exchanges was many $M per day, creating an opportunity for the company or any token holder to convert their LBC into bitcoin or real dollars. This opened up the possibility of using tokens to attract new customers, to acquire content rights, even to compensate employees and contributors.

We’ve Entered a New Era of Building and Financing Companies

It dawned on us that we had entered a new era of building and financing companies.

- The idea of giving users of a network the opportunity to share in the value appreciation of the network by owning tokens is a big idea.

- Pre-selling tokens as a way to fund your company is a big idea.

- Using tokens on an ongoing basis to provide incentives to new users and to attract partners is a big idea.

Most venture capital firms were not created with the idea of owning crypto tokens and ours is no exception. We convened our Advisory Board (essentially our Board of Directors, populated by entrepreneurs and experienced leaders from some of the nation’s top VC firms) to discuss the changes we were seeing in the market. Namely, in this crypto world, it was no longer clear whether value would be built in the equity or the token.

Should we stick to our knitting and buy equity or dare we start buying tokens directly?

Buying Equity has Benefits

- Alignment — we are aligned with the founders. Founders typically own equity and don’t have direct ownership of tokens either. If they were to receive tokens, it would be because the company decide to distribute them to shareholders — all of us, proportionately.

- Flexibility — investing in equity allows us to stay aligned with founders as the company’s business model evolves. For instance, if the company had a problem with the first token and needed to issue a replacement — or if they decided to launch a second token with a new function. If we owned that now defunct, token, we’d be in deep trouble. If we were equity owners, we are insulated from these machinations. Buying equity keeps us in lock-step with the founders as the company twists and turns.

- Visibility and Control — equity investments typically come with information rights and other financial and control terms. This wasn’t particularly important to us, as our firm prefers to buy common stock in companies (to put us on equal footing with founders), so we don’t expect or require the typical protections a venture investor would usually want (preference, anti-dilution,, dividends, etc.). This might be important to some, but is less so to us.

Buying a SAFT Does Too…

Buying tokens via a SAFT (simple agreement for future tokens — a security that converts into tokens) has a primary benefit as well, namely:

1) Liquidity — One of the most interesting aspects of crypto investing is that liquidity may not take the standard 5–7 years it does in a “normal” startup investment. In the case of LBRY, there is a liquid market for the token — and the company owns many $M of tokens — but as equity investors, we need to wait for a dividend or distribution. Buying tokens directly here would give us the fastest path to liquidity.

There are significant advantages on both sides. Equity provides flexibility, tokens provides faster liquidity.

Are Economics the Tie Breaker?

If we are buying equity, we own a piece of a company with several potential sources of value:

- Value of tokens owned by the company

- Value of any cash flow associated with transaction fees and advertising on the network

Token value — our token value will be equal to our portion of the company owned tokens. But what portion of all tokens will the company retain?

The typical breakdown is:

- 50% sold to ICO buyers

- 25% reserved for incentives to acquire customers and reward partners

- 25% retained by the company.

If the company ends up retaining 25% of all tokens post ICO and we “own,” for instance, 20% of that equity, we have an effective of 5% (20% of 25%) of all outstanding tokens. This was an important realization — 3/4ths of the tokens will be sold or given to 3rd parties, so even though we own 20% of the company, we only “own” 5% of the tokens.

We say “own” because the tokens aren’t really ours — they are an asset of the company and stay on the company’s balance sheet until management decides to distribute to shareholders (investors, founders, employees).

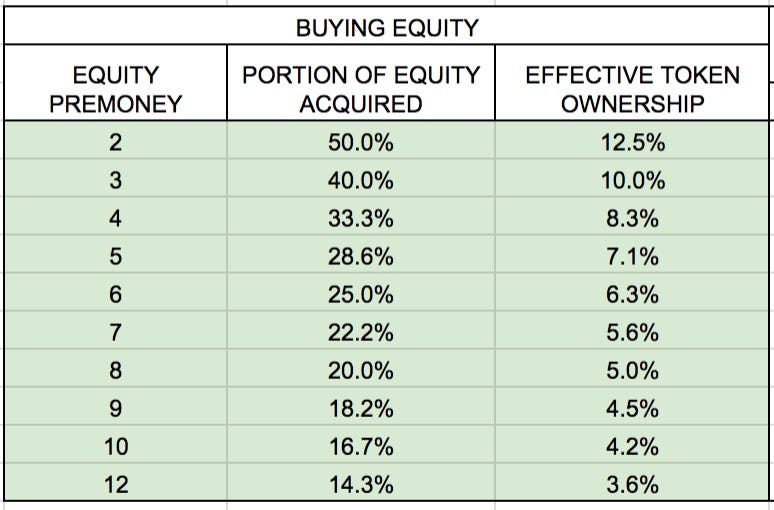

What’s the effective token ownership of, for instance, a $2M investment in equity? Its a function of the pre-money.

As equity owners, the key is understanding what portion of the tokens a company will retain, and under what circumstances they will distribute to shareholders.

Transaction fees and advertising are other promising sources of value. We think transaction fees are under appreciated in the current environment and over time, more networks will take modest fees to fund ongoing product development and operating costs. Advertising also has a big potential role to play if done in a way that is viewed as improving the user experience.

In this simplified analysis, we are looking solely at the value of the tokens themselves. This is a conservative view and any transaction or advertising fees would be upside to this case.

If we are buying tokens, we are typically getting a discount to the ICO price of 25–50% depending on how early we entered. The earlier the investment, the bigger the discount.

Buying tokens in a pre-sale or SAFT is a lot like buying equity in a traditional company through an uncapped note with an discount to the next round.

In the token world, that next round is the ICO — and as mentioned earlier, ICO buyers are typically buying 50% of the tokens in the ICO process. This means that ICO proceeds and ICO pre-money track very closely. If ICO proceeds are $15M and buyers are purchasing 50% of the tokens, they are valuing the network at $15M pre-money, $30M post-money.

The portion of tokens our same $2M buys is show below as a function of ICO size. Here we assume we are getting a 35% discount to the ICO price. As you can see, the larger the ICO, the smaller proportion our $2M buys. This is because the “pre-money” tracks to the size of the offering, and our price is a 35% discount to that pre-money.

And now we can compare apples to apples — at least on a token basis. We’ve made each row show equal “token ownership” — so you can see that a $2M equity investment at $8M pre money valuation is equivalent to buying $2M in tokens (at a 35% discount) followed by a $31M ICO.

Looking at this chart is quite revealing. For instance, the 2nd row. Investing $2M into a SAFT, at a 35% discount for a company planning on doing an ICO of $15M is equivalent to buying $2M of equity of the company at $3M pre-money. We don’t see very many deals at $3M pre-money for equity so this looks like very compelling — for investors.

We found this surprising — and suspect many founders would feel the same way.

What’s the summary of all of this?

- Buying equity has advantages in terms of alignment and flexibility.

- Buying tokens has the advantage of early liquidity for investors.

- Buying tokens is often the better economic deal for investors

Conclusions

Despite the opportunity for early liquidity and the better economic case, we have a strong preference for buying equity. The core thesis of our fund is alignment with entrepreneurs and we continue to believe that buying equity is the best way to achieve this goal. It is hard enough to build a valuable company when everyone is pulling in the same direction, why would we want to enter a structure that could put us at odds with founders and employees. This is particularly important where the situation is fluid — the future is uncertain and companies may have to evolve due to changing regulatory, market or technical reasons. That pretty much defines today’s crypto market.

This review has also reinforced that whether buying equity or tokens, we had better convince ourselves of the value of the network itself and the growing demand for tokens. We’ll share our thinking in a future post.

In the meantime, we’d love to hear your feedback.